WHAT YOU NEED TO KNOW

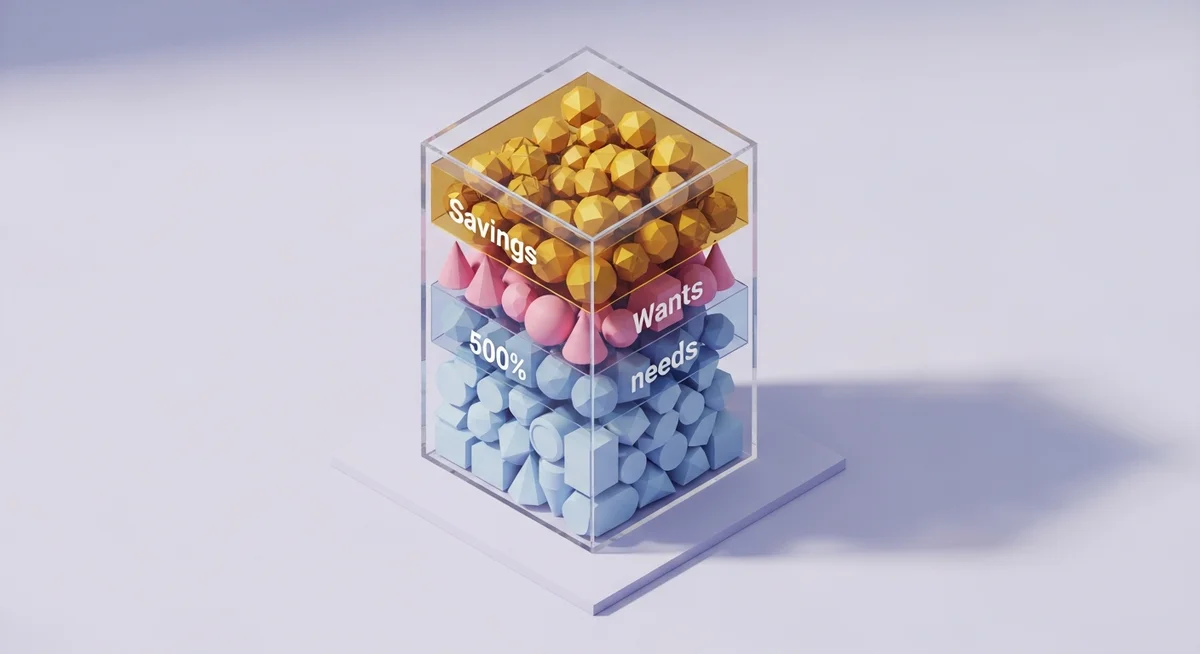

The 50/30/20 budget rule is a highly effective, low-friction financial framework that splits your take-home pay into three simple categories: essentials, lifestyle spending, and future goals.

- It allocates 50 percent of your net income to your essential living needs, ensuring your core survival expenses are covered first.

- It reserves 30 percent for discretionary choices, allowing you to enjoy your money without guilt or constant tracking.

- It dedicates the final 20 percent to building an emergency fund, investing for retirement, or paying off debt ahead of schedule.

With The 50/30/20 Budget Rule Explained, you can easily organize your take-home pay without tracking every single transaction, though your actual percentages may require adjustments depending on your local cost of living and current debt burdens as of 2026.

The 50/30/20 Budget Rule Explained: What Is It?

The 50/30/20 budget rule is a straightforward money management template designed to simplify how you divide your monthly income. Originally popularized by financial experts and policymakers, this method eliminates the tedious task of tracking every single penny by grouping your money into three broad buckets.

- 50 percent for Needs: Your mandatory bills and survival essentials.

- 30 percent for Wants: Your lifestyle choices, dining out, and entertainment.

- 20 percent for Financial Goals: Your savings, investments, and extra debt payments.

By using percentages rather than rigid dollar limits, this framework scales naturally as your income changes. It provides a balanced approach that ensures you plan for the future while still enjoying the present.

Breaking Down the 50/30/20 Categories

50%: Needs (Your Essentials)

Needs are the absolute requirements you must pay to keep your household functioning and avoid financial default. According to consumer guidelines from the Consumer Financial Protection Bureau (CFPB), failing to meet these mandatory obligations can severely damage your credit health and financial stability.

- Housing costs: Your rent payments, mortgage payments, and basic property taxes.

- Utilities: Electricity, heating, gas, water, and essential phone or internet service.

- Transportation: Fuel, public transit passes, car insurance, and minimum car loan payments.

- Minimum debt payments: The absolute minimum required payments on credit cards, personal loans, or student loans.

- Groceries: Basic food supplies and household necessities, excluding premium dining out or specialty treats.

30%: Wants (Your Lifestyle choices)

Wants are the things that enhance your quality of life but are not strictly necessary for survival. You can temporarily cut these expenses to zero if you experience a sudden loss of income or a personal emergency.

- Entertainment: Movie tickets, concerts, sporting events, and streaming subscriptions.

- Dining out: Restaurant meals, takeout, bar tabs, and expensive daily coffee trips.

- Travel and leisure: Weekend trips, seasonal vacations, and hobby equipment.

- Upgrades: Buying a premium smartphone when your current device works perfectly, or purchasing designer clothing.

20%: Savings and Debt Repayment (Your Financial Goals)

This final category is the foundation of your long-term security and wealth. While your mandatory minimum debt payments live in the 50 percent bucket, any extra principal payments you make to accelerate your debt payoff belong right here.

- Emergency savings: Building a liquid financial cushion of three to six months of living expenses.

- Retirement accounts: Contributions to a workplace 401k or an Individual Retirement Account (IRA).

- Extra debt payments: Additional payments made directly to the principal on high-interest credit cards, car loans, or student loans.

- Down payments: Saving cash for a home purchase, a car purchase, or other major future assets.

How to Set Up Your 50/30/20 Budget

Step 1: Calculate Your Net (Take-Home) Income

You must base this budget on your net income, which is the money that actually lands in your bank account. If your salary is paid hourly or monthly, look at your net pay stubs after taxes, Social Security, and workplace health insurance premiums have been deducted. For example, if your gross salary is $4,000 per month, but after federal, state, and payroll tax deductions you receive $3,000 in your bank account, your budgeting starting point is exactly $3,000.

Step 2: Map Your Expenses Into the Three Categories

Once you know your net income, you can multiply it by the percentages to find your monthly target limits. Let us continue with our concrete example of a monthly net income of $3,000 to show how this works in practice.

- Needs (50 percent): $3,000 multiplied by 0.50 equals $1,500 per month for essentials.

- Wants (30 percent): $3,000 multiplied by 0.30 equals $900 per month for lifestyle choices.

- Savings and Debt (20 percent): $3,000 multiplied by 0.20 equals $600 per month for financial goals.

Step 3: Track and Adjust Your Monthly Spending

Review your actual spending from the previous 30 days to see how closely your current lifestyle aligns with these calculations. If you find your current spending exceeds the target limits, look for small adjustments in your variable expenses to restore balance. You do not need to track every penny forever, but checking in once a month ensures your spending habits match your financial priorities.

Real-World Flexibility: Customizing the Percentages to Fit Your Life

While the standard percentages work well for many people, they are not rigid rules written in stone. If you live in a high-cost-of-living area, your housing costs might easily push your essentials above the recommended limit. The Federal Reserve reported that rising housing costs have forced many consumers to adjust their monthly budget allocations to fit their local realities.

You can customize the split to match your current season of life by using these common variations:

- The 60/20/20 Split: Designed for high-cost-of-living areas where basic rent and utilities consume 60 percent of your income, leaving 20 percent for wants and 20 percent for savings.

- The 70/20/10 Split: Ideal for people living paycheck to paycheck who must dedicate 70 percent of their net pay to essentials, leaving 20 percent for wants and 10 percent for savings.

- The 50/10/40 Split: For aggressive savers or debt-builders who choose to minimize their lifestyle wants to just 10 percent to accelerate their financial goals.

Pros and Cons of the 50/30/20 Rule

Understanding the strengths and limitations of this system can help you decide if it matches your financial personality.

| Pros | Cons |

|---|---|

| Simple to understand and implement for beginners | Can be unrealistic in high-cost-of-living areas |

| Flexible and easily customizable to fit your life | Does not provide detailed transaction tracking |

| Prioritizes savings and extra debt repayment automatically | Might feel too loose for aggressive savers |

| Allows guilt-free spending on lifestyle wants | Blurs the line between needs and wants occasionally |

Alternatives to the 50/30/20 Budget Rule

If this percentage-based system does not suit your style, there are several other practical methods you can explore. The key is to find a system that keeps you consistent and protects your financial peace.

- Zero-Based Budgeting: This method gives every single dollar a specific job so your income minus your expenses equals zero at the end of the month.

- The Cash Envelope System: A physical budgeting method where you place cash into labeled envelopes for groceries, entertainment, and other variable expenses to prevent overspending.

- The Pay-Yourself-First Rule: A reverse budgeting strategy where you immediately transfer money to your savings and investment goals the moment you are paid, then spend the remainder of your check freely.

For additional support and strategies to improve your financial habits, you can explore the educational guides at Payday Advisors to help guide your budgeting journey.

Frequently Asked Questions About the 50/30/20 Rule

Do I calculate my budget using gross or net income?

You should always calculate this budget using your net income, which is your actual take-home pay after taxes and mandatory workplace deductions. If you use your gross income, you will over-allocate money to your needs and wants, leaving yourself with less cash than you actually have in your bank account.

Is debt payoff classified as a “Need” or “Savings”?

Debt payoff is divided between both categories depending on the size of your payment. Your minimum monthly debt payments are classified as a “Need” because failing to pay them will hurt your credit score and invite collection actions. Any extra payments you make on top of the minimum to get out of debt faster are classified as “Savings” because they directly build your future wealth. The Federal Trade Commission (FTC) provides resources on managing collections and debt if you struggle with minimum payments.

What if my rent/mortgage already takes up more than 50% of my income?

If your basic living expenses exceed the 50 percent limit, do not panic or abandon budgeting. You can temporarily adjust your framework to a 60/20/20 or 70/20/10 split while you work to increase your income or look for ways to trim your fixed costs over time.

What if I cannot afford to save 20% right now?

Start exactly where you are today, even if you can only afford to save 5 percent or 10 percent of your income. The habit of saving consistently is far more important than meeting the perfect target right away, and you can slowly increase your savings rate as your financial situation improves.